November’s unemployment report contained the typical assortment of good news and bad news.

The good news was in the headline. The unemployment rate fell to 4.2% — well below its 70-year average of 5.8%.

The bad news is in the participation rate. The rate rose to 61.8%, which is above the pandemic low of 60.2% but is still well below the pre-pandemic level of 63.4%.

This highlights the problem that millions of people are not interested in working. As Barron’s explained: “Millions have remained out of the workforce for longer than economists and policymakers have anticipated, defying widespread expectations for a mass return to work in the fall when in-person school resumed and generous unemployment benefits expired.”

There is hope that higher wages and a record number of job openings will attract some back to the labor force. But the amount of the working-age population not interested in working is troubling.

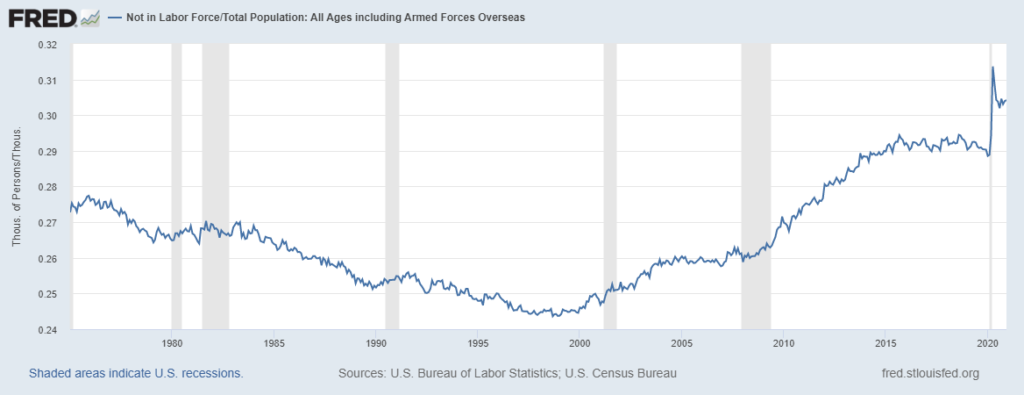

Less Workforce Participation Means Slower Growth

The chart below shows the percentage of people not in the labor force as a percent of the population.

Percentage of the Population Not in the Workforce

Source: Federal Reserve.

As the Bureau of Labor Statistics notes: “Persons who are neither employed nor unemployed are not in the labor force. This category includes retired persons, students, those taking care of children or other family members, and others who are neither working nor seeking work.”

Many of these individuals are out of the workforce for good reasons — perhaps all of them are — but that is still a factor that policymakers should worry about.

Right now, 30.4% of the population is not in the labor force. The economy is the sum of the economic output of all workers. Nonworkers slow the pace of economic growth.

In time, the economy should be able to adapt to a higher percentage of potential workers sitting on the sidelines. But that can take years. In the short run, this is a drag on economic growth that adds to inflationary pressures since output is lower than it could be.

Policymakers need to address this issue, but it’s a challenging problem.

Michael Carr is the editor of True Options Masters, One Trade, Peak Velocity Trader and Precision Profits. He teaches technical analysis and quantitative technical analysis at the New York Institute of Finance. Follow him on Twitter @MichaelCarrGuru.

Click here to join True Options Masters.