If you’re looking for quality yield on your investments, a real estate investment trust, or REIT, has traditionally been a good place to look.

But the coronavirus significantly changed the landscape for real estate.

Now, owning the wrong REIT can be a costly endeavor.

So here we’ll show you a REIT to buy right now … and one to steer clear of.

What is a REIT?

In simple terms, a REIT is a company that owns, operates or finances income-generating real estate.

The company pools the capital of many different investors, similar to that of a mutual fund.

Investors earn dividends from real estate investments without actually owning, managing or financing property themselves.

REITs are usually specific to a sector, such as data centers, hotels and apartment complexes.

There are also REITs that are more diversified to include office and retail properties.

They are mostly traded on major securities exchanges like any other stock. REITs are typically quite liquid and trade a lot of volume.

Under the Internal Revenue Code, here are the requirements for what constitutes a REIT:

- Invest at least 75% of total assets in real estate, cash or U.S. Treasurys.

- Derive at least 75% of gross income from rents, interest on mortgages that finance real property, or real estate sales.

- Pay a minimum of 90% of taxable income in the form of shareholder dividends each year.

- Be an entity that’s taxable as a corporation.

- Be managed by a board of directors or trustees.

- Have at least 100 shareholders after its first year of existence.

- Have no more than 50% of its shares held by five or fewer individuals.

What Has Changed in the REIT Market?

When the coronavirus first took hold, state and local governments shut down the economy by requiring people “shelter in place” and stay home to help prevent the spread.

The underlying consequence was that rents on offices, apartments, restaurants and other properties were either not paid or negotiated down.

That cut into the taxable income a REIT provides to investors in the form of dividends.

But it’s not all bad news.

The U.S. economy is starting to reopen.

Businesses are opening their doors to customers and employees are returning to work.

We are starting to see a degree of normalcy return to business activity we haven’t seen in more than two months.

That’s why one of these REITs is a solid investment right now. As the economy continues to open, rents will get paid and dividends will start to grow.

That’s why we’ll show you one REIT you should buy right now, and the REIT you should avoid.

A REIT to Buy: This Life Science REIT Capitalizes on Health Care

Over the course of the coronavirus pandemic, the stock market saw a massive dip in February into March.

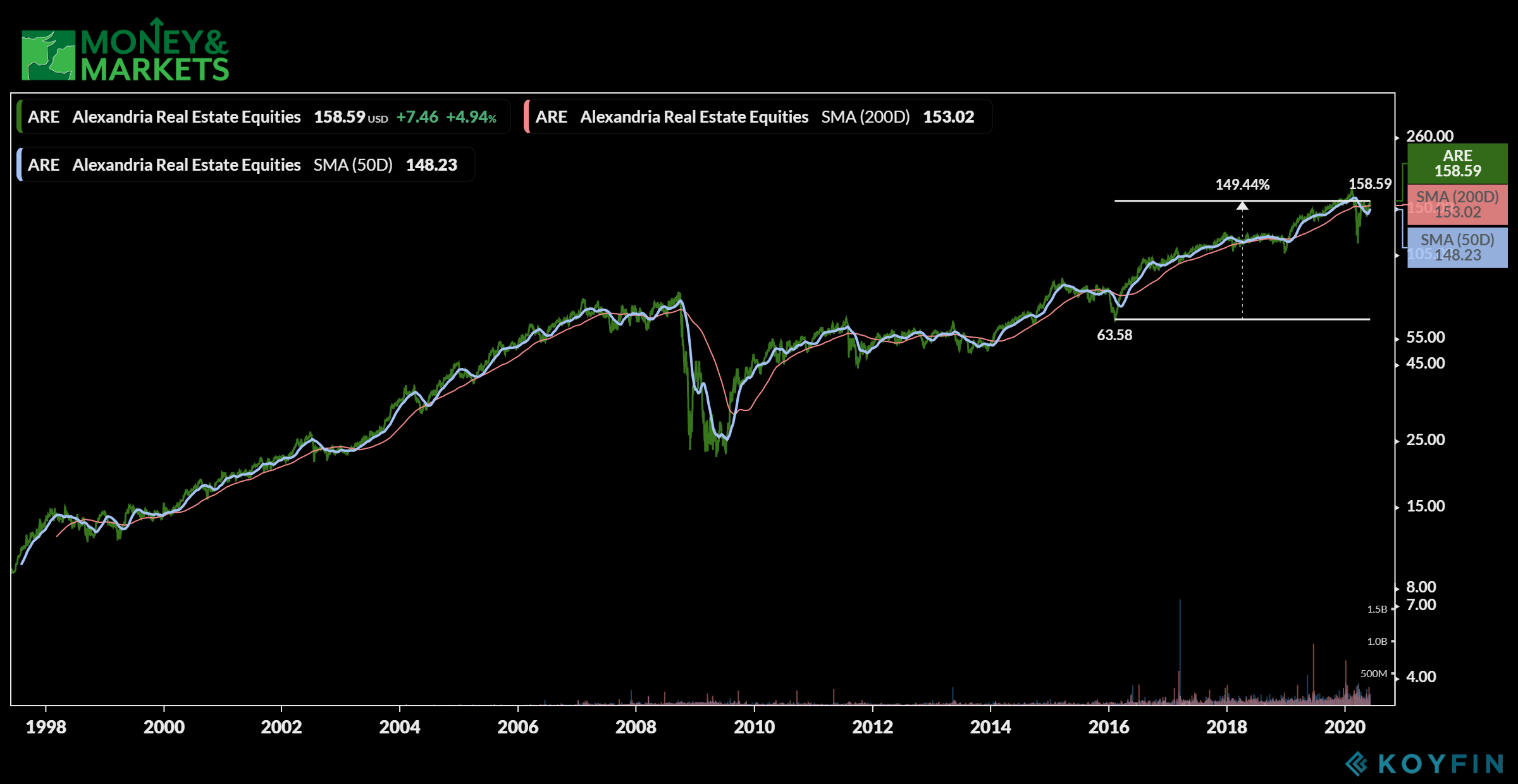

The Alexandria Real Estate Equities REIT (NYSE: ARE) saw a dip, but not until after the rest of the market had already dropped.

Now the REIT that specializes in owning, operating and managing pharmaceutical, biotechnology and life science properties is back on the move upward.

It’s trading at around $158 per share and momentum indicates is could reach its 52-week high in short order. It’s also trading just above its 200- and 50-day moving averages — a threshold it only recently crossed.

Unlike other REITs, Alexandria maintained its dividend payments — $1.03 per share in the last two quarters — and actually increased it over last year.

Alexandria is moving upward and picking up where it left off before the coronavirus pandemic kicked in.

That makes it a REIT to buy now.

This Entertainment REIT is One to Avoid Right Now

The entertainment industry has been rocked by the pandemic.

And it’s likely to continue to suffer even when the economy fully opens back up.

People are going to be hesitant about going to a packed movie theater or an “eat and play” restaurant.

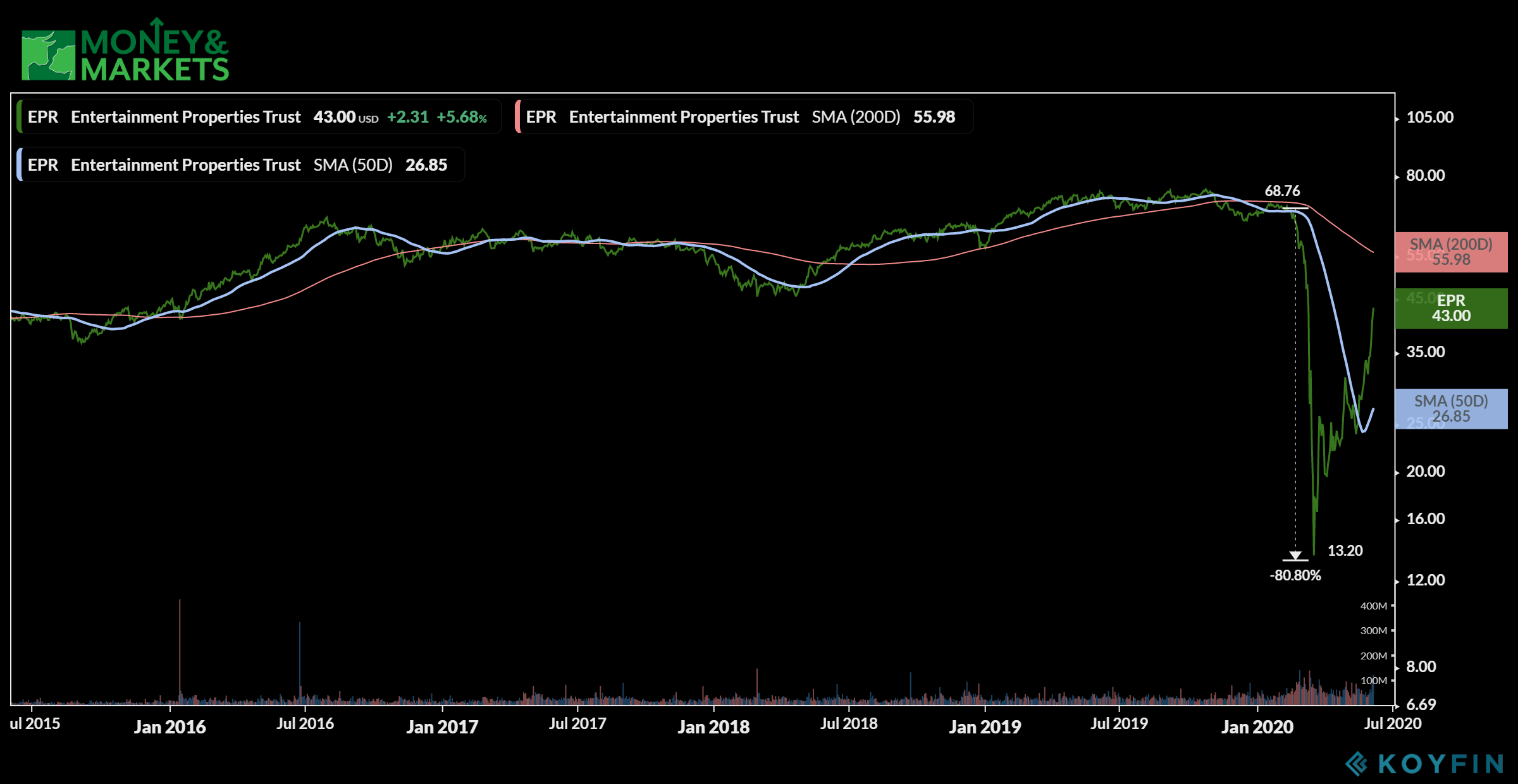

That’s why Entertainment Properties Trust (NYSE: EPR) is a REIT you will want to avoid for the time being.

It specializes in large movie theater complexes, entertainment retail centers and destination recreational properties.

This REIT suffered a staggering 80% drop in share price — down to $13.92 per share — in March. On top of that, it only collected about 15% of its rent in April.

You can see the stock has started to rebound, but it is still well below its 200-day moving average.

It does pay a monthly dividend — about $0.38 per share in the last two months — and that was an increase from the previous months. However, I suspect that was to keep investors interested and not necessarily a reflection of increased profits.

But, with the prospects of a recession, consumer discretionary spending could taper off. That will leave EPR with a lot of customers with much lower income and a higher risk of default, making it a REIT to avoid for the time being.