This selloff has set up a very rare opportunity to bag yields of at least 12% in closed-end funds (CEFs). I’ll reveal three names and tickers you’ll want to target now in just a second.

This chance to kickstart a steady income stream exists because CEF buyers are a conservative bunch, so these funds’ downdrafts have been amplified this year. (This also means that income-hungry CEF buyers tend to buy back in quickly, driving these funds to fast upside after a drop).

The upshot here is that all 500 or so CEFs in existence are sporting an average discount to net asset value (NAV, or the value of their underlying portfolio) of 7.5% — making them cheaper than they’ve been in nearly a decade.

That’s giving us our “in” on these income wonders, many of which pay dividends monthly.

While some CEFs deserve their discounts because of bad management, there are many more that have weathered past selloffs and come out stronger.

The three funds below are good examples of resilient CEFs, with the income they’re collecting from their portfolios continuing to cover their own high payouts to us. Their holdings also give us an attractive mix of safety and growth, with exposure to blue chip stocks, bonds, utility stocks, energy stocks and beaten-down tech stocks that are overdue for a bounce.

CEF Pick No. 1: An Oversold Bond Fund With a “2022-Proof” 15.1% Payout

Let’s start with the Virtus Convertible & Income Fund (NYSE: NCV), which boasts an incredible 15.1% dividend yield as I write this.

NCV funds that hefty payout, which has held up through the darkest days of 2022, with a mix of corporate and convertible bonds that tend to be less volatile than stocks. What’s more, NCV pays dividends every single month.

NCV funds that hefty payout, which has held up through the darkest days of 2022, with a mix of corporate and convertible bonds that tend to be less volatile than stocks. What’s more, NCV pays dividends every single month.

Source: Virtus Investment Partners.

NCV’s 60% allocation to convertible securities (which can be converted from bonds to stocks when certain benchmarks are met) is important for another reason: these assets tend to have higher yields than regular corporate bonds. For example, NCV’s top three holdings are convertible issues from Wells Fargo, Bank of America and Broadcom yielding 7.5%, 7.25% and 8%, respectively.

The best part about NCV is that it trades at a 13.8% discount to NAV as I write this, well below its 52-week average of a 6.9% discount. That suggests considerable upside for the fund as it returns to that more “normal” level.

CEF Pick No. 2: A 14.9% Payer That’s Built for Inflation and Recession

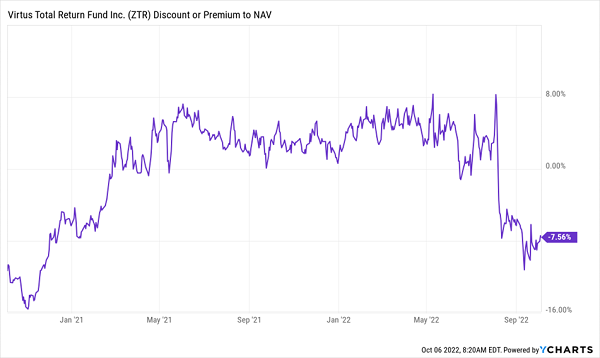

Next let’s take the 14.9%-yielding Virtus Total Return Fund Inc. (NYSE: ZTR), which typically trades at a premium but has seen its pricing collapse in recent months. It now trades at a discount the likes of which we haven’t seen for two years.

Another Big Sale Appears

The fund’s portfolio is the main source of the premium valuation it earned until now. Its holdings are nicely set up for the inflation we’re dealing with now and the recession we may be dealing with next year, with half of its investments in utilities, a third in industrials and the rest in energy, real estate and other sectors. (Energy and utilities are the only sectors that are up over the past year, and industrials are one of the better-performing sectors of the last three months).

Market dominators like cell-tower owner American Tower Corp. (NYSE: AMT) and renewable-focused utility NextEra Energy Inc. (NYSE: NEE) populate ZTR’s portfolio.

This attractive mix of holdings has attracted income seekers to ZTR, until the recent market pullback deterred them, opening up the fund’s discount for us.

CEF Pick No. 3: A “Contrarian’s Choice” CEF That Pays 12.3%

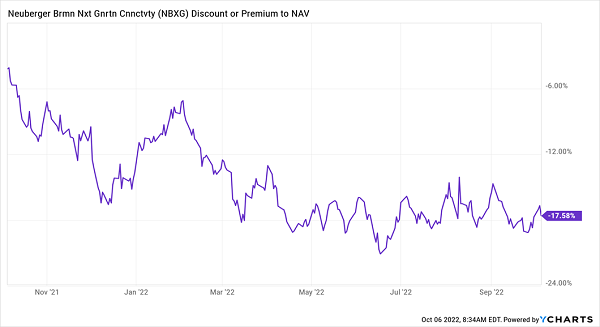

On top of energy, utilities, and bonds, we need some growth. While growth stocks, especially tech, have been hit harder than any other sector in the sell-off, that also means these firms have the most upside. We can get those oversold assets in the shape of an oversold fund if we buy the Neuberger Berman Next Generation Connectivity Fund (NYSE: NBXG).

NBXG: An Oversold Fund With (Absurdly) Oversold Assets

The fund’s 17.6% discount made it one of the most oversold funds on the market, which also means its 12% yield has become more sustainable.

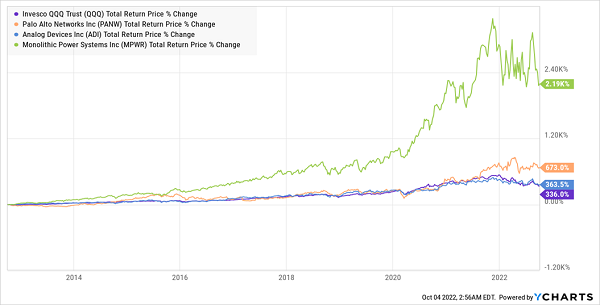

That’s because the fund’s 12% yield is based on its discounted market price. When you calculate its dividend as a percentage of NAV, it comes out to 9.9%, and a 9.9% annualized return over the next decade is very attainable for the high-tech firms NBXG owns, like Palo Alto Networks Inc. (Nasdaq: PANW), Analog Devices Inc. (Nasdaq: ADI) and Monolithic Power Systems Inc. (Nasdaq: MPWR). This chart explains why.

Big Returns From Market Lows

Even accounting for the recent sell-off, NBXG’s top holdings have crushed the tech-focused NASDAQ 100 index, providing average annualized returns of 26.6% over the last decade.

Those returns aren’t surprising: New technologies fuel economic growth more than anything else, and firms that provide those technologies benefit accordingly. NBXG is an opportunity to get those firms at a big discount while the market is panicking over the Federal Reserve’s interest rate hikes, which futures markets predict will halt in a few months anyway.

To learn more about generating monthly dividends as high as 8%, click here.