We’re now two weeks out from the moment the United Kingdom left the European Union. The culmination of more than 25 years of work by Nigel Farage and the people he inspired, Brexit stands as one of the most important geopolitical events of the century.

The political elite in Brussels refuse to admit it publicly but they are now staring at a disaster without the U.K. to suck dry. Net of U.K. transfer payments each year, the EU budget has to come up with a $13.2 billion hole that it can’t plug without raising taxes.

At the same time, everyone who is anyone in Brussels is talking about a massive Keynesian-esque spending program to combat climate change. But the EU has no capacity to pull off this stunt without sincere changes to its legal and monetary infrastructure.

The shenanigans last week in Thuringia, which I covered here, amount to a political earthquake in Germany that calls into question its ability to set the legislative agenda when Germany assumes the Presidency of the European Commission in July. Chancellor Angela Merkel is losing control of both her party, the Christian Democratic Union (CDU), and her ruling coalition with the Social Democrats.

The potential for a lurch to the right within the CDU sets the stage for a collapse of Germany’s government later this year.

And this is having huge effects on the euro. Since the end of January where markets mysteriously bounced to support the euro and trash the U.S. dollar, we’ve seen the exact opposite trade emerge since the markets opened in February.

The euro has collapsed. There’s no other way to put it.

It began the moment China’s markets reopened. Escalating fears over the extent the coronavirus is affecting day-to-day life in China’s biggest industrial cities has created a massive safe-haven trade across all asset classes.

Europe’s political dysfunction and paralysis cannot compete with these growing fears.

The Fed continues to fight rising short-term interest rates in the repo markets, even though it is trying to taper off its involvement. Foreign investors can’t seem to get enough of U.S. treasury debt with blistering 30-year and 10-year auctions this week.

The Treasury auctioned off $19 billion in 30-year bonds at the lowest yield on record at 2.068%.

Gold’s correction is over as it grinds toward $1,600 per ounce and the entire cryptocurrency market has been on fire with Bitcoin (BTC) making headlines this week re-crossing $10,000 per coin for the first time since last fall.

At the same time, stocks continue to confound analysts who see these black swans and cannot comprehend that stocks, especially U.S. stocks, are safe-haven assets when they are yielding around the same as a 30-year U.S. treasury bond.

Let’s explore this thesis a little further. If you’re a German investor are you ploughing money into German 10-years at -0.39% or the German DAX at yielding 2.5% according to the 12 month trailing yield of the Global X German DAX ETF (NASDAQ: DAX)?

You can either make around 1.5% in real yield on German stocks, even if the German economy is close to contraction, or you can lose around the same amount buying German government debt?

The choice seems clear to me.

And with a crashing euro the implied yield on that German debt continues to fall. At this point what’s keeping the European sovereign debt market in place is the continued pledge by the ECB to buy it, allowing momentum traders to front-run the ECB in the hopes of picking up nickels in front of a freight train coming the other way.

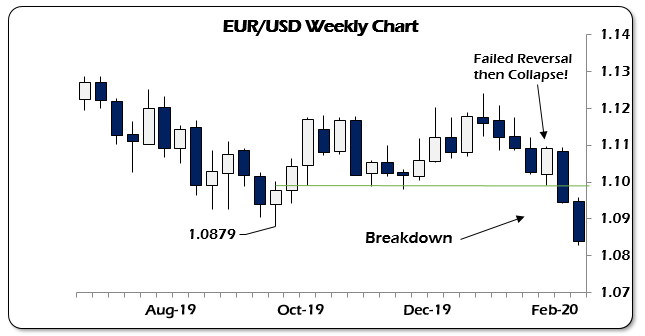

Here is the weekly chart of the Euro.

The euro’s inability to follow through in February negated any chance of a stabilizing rally. It calls into question the strange behavior of markets on Brexit day. And since then, at least in the currency markets, fundamentals are asserting themselves and with a vengeance.

The knock-on effect of this is part of what’s driving the push by major stock indices to new highs. I’ve been warning since the year began that the weakness in the U.S. dollar to end 2019 was temporary and that call has been spot on.

What’s worse for Europe is that its leadership seems oblivious to the problems it is facing. Chief Brexit negotiator Michel Barnier’s ostrich-like behavior has him making the same demands of the U.K. in trade deal talks which the three-plus-year Brexit fight ultimately rejected.

The European project is burning down in front of our eyes and the markets will ultimately make them pay for their inability to overcome the deep political divisions which plague it. The mistake was in pushing for this political union that no one in Europe signed up for willingly, except the politicians and oligarchs that promoted it.

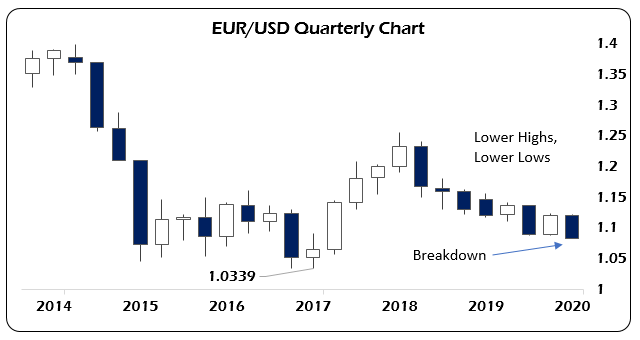

Now we have our signal that the markets reject the idea they can keep the forces tearing at the seams of the EU from unraveling. If markets still believed that, they wouldn’t be driving the euro toward its five-year low like someone stole it.

This price action is a classic example of how short-term technical signals can propagate out in time. A weekly reversal signal that breaks a previous monthly low which also breaks a quarterly low implies that this short-term price action has broad significance that investors (and frankly regulators) ignore at their own peril.

Currency prices are a reflection of the political stability of the country issuing that currency. The EU isn’t the only country issuing euros. And that’s the fundamental problem. Watch the headlines coming out of Germany closely. The fireworks may be over for now but there’s still embers smoldering which are waiting to set off the next round of chaos there.

But the one thing I can assure you of, the people in charge of things there do not know how to put the fire out.