It’s been a week of big stock moves in the market.

Every day, I open Bloomberg to see another company’s stock swing higher or lower after headline news.

Some of the highlights include:

- Trading on Trump Media (Nasdaq: DJT) stock was halted after double-digit swings both higher and lower.

- A 20% drop for Estee Lauder Companies Inc. (NYSE: EL) on Thursday after the company disappointed on earnings and cut its dividend.

- On the other hand, Paycom Software Inc. (NYSE: PAYC) soared 23% on Thursday after beating earnings expectations and providing strong guidance for the future.

That was just on Thursday!

When I see stock prices rising or falling rapidly after an earnings report or other headline story, I like to open up Green Zone Power Ratings to know where that stock stands in Adam O’Dell’s system.

One-day moves are great, but buying a stock after a big move, only to see it not go higher (or even decline) is an awful feeling.

So, let’s see how two other big movers from this week stack up…

SMCI’s AI-Fueled Rally Has Fizzled

The artificial intelligence (AI) mega trend is well underway, but headwinds are forming after the initial bullish charge for certain AI-related stocks.

One company that’s been in the headlines for all the wrong reasons lately is Super Micro Computer Inc. (Nasdaq: SMCI).

As you may know, AI tech relies heavily on data centers. These facilities house thousands of physical servers, which allow AI to process and spit out results in the blink of an eye. Super Micro builds server racks that help cool equipment involved in these processes. It’s a sort of picks-and-shovels stock for the AI revolution. And SMCI stock has gone gangbusters thanks to its competitive edge.

But all is not well…

On Wednesday, a filing revealed that Ernst & Young had resigned as one of Super Micro Computer’s auditors. This comes two months after Hindenburg, a prominent short-selling firm, reported it had “found glaring accounting red flags, evidence of undisclosed related party transactions, sanctions and export control failures, and customer issues” as part of a three-month investigation into Super Micro.

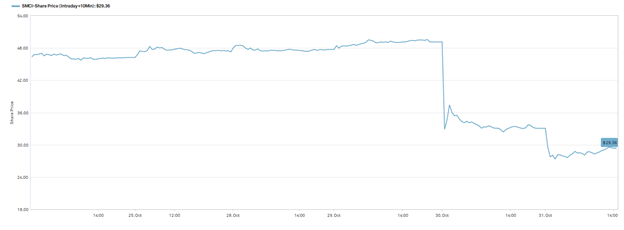

SMCI stock had already been in decline since March, but the stock went into freefall on Wednesday. Between Tuesday’s close and midday Thursday, SMCI lost 40% of its value.

SMCI’s Snap Crash

Was Green Zone Power Ratings already waving the red flag on SMCI?

Yup…

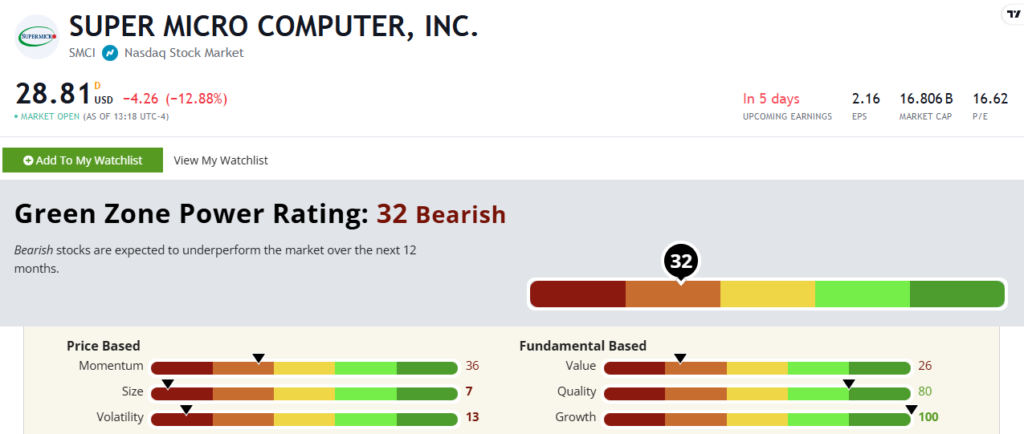

SMCI’s Green Zone Power Ratings in November 2024.

Super Micro stock rates a “Bearish” 32 out of 100, which means it’s expected to underperform the market over the next year.

A 100 rating on Growth is impressive. The company’s latest earnings report noted a 142% increase in year-over-year revenue to $5.3 billion, which is massive. Quality is also good, with Super Micro reporting $343 million in operating income, a 51% increase from a year ago.

But this has all the markings of an overbought tech stock. Low value ratings show that current valuations can’t support its inflated stock price.

Year to date, SMCI stock has gained a slight 3%, but that doesn’t tell the whole story. Since hitting a 52-week high of $122.90 back in March, the stock has shed 75% of its value and now trades just north of $29. That’s why it only rates a 36 on Momentum now.

And with big moves following Hindenburg’s report and EY’s exit, you can see why it rates a 13 on Volatility.

A flurry of rough news and poor Green Zone Power Ratings have me pressing pause before buying any dips. (Chief Research Analyst Matt Clark reached the same conclusion recently.)

Let’s see if there’s a more positive story out there…

GRMN’s 20% Pop Amid a Quiet Rally

I’ve written about Garmin Ltd. (Nasdaq: GRMN) a few times in Money & Markets Daily. I like the company’s products, and I think its stock has a lot of promise for the future.

So I had a slight grin on my face when I logged into work on Wednesday and saw that GRMN had surged more than 20% higher following a blockbuster earnings report.

Of course, Green Zone Power Ratings has been on top of it for a while now:

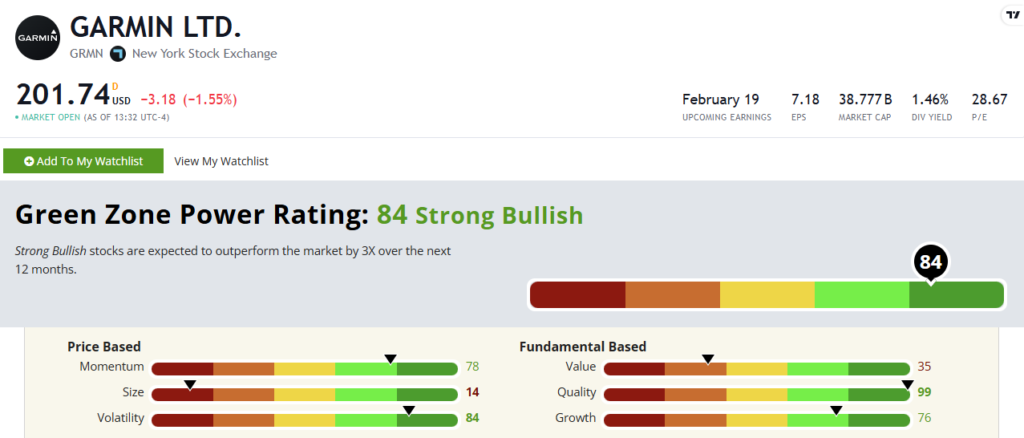

GRMN’s Green Zone Power Ratings in November 2024.

GRMN stock rates a “Strong Bullish” 84 out of 100, which means it’s expected to 3X the broader market over the next year.

For a glimpse into its strong Growth ratings, we just need to look at that latest earnings report. Garmin beat on both earnings per share (EPS) and revenue for the third quarter of 2024:

- $1.99 EPS reported vs. $1.44 expected.

- $1.59 billion in revenue compared to $1.44 billion expected.

Garmin also raised its full-year profit and revenue forecasts, citing stronger demand for its wearables than what was initially expected. American consumers are spending, and a lot of them are buying Garmin smartwatches (guilty!).

I’ve mentioned it in the past, but this is a tech stock that’s flying under the radar. While investors are looking for the next Magnificent Seven or a glitzy AI stock, GRMN has gained almost 100% over the last year, nearly tripling the S&P 500’s 36% gain. That’s why it boasts a 78 rating on Momentum.

With strong guidance for the future and a “Strong Bullish” score in Green Zone Power Ratings, GRMN definitely looks like a stock with legs to run higher. (Sorry, I had to squeeze in one more lousy running pun.)

Until next time,

Chad Stone

Managing Editor, Money & Markets

P.S. Thank you, Courtney C. for the suggested nickname of “Tank 2.0” for my newest Garmin watch. I think it’s a nice fit! If you ever have a suggestion or question about Money & Markets Daily, reach out to Feedback@MoneyandMarkets.com.